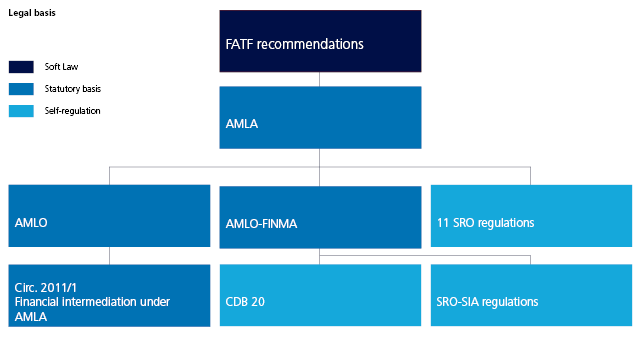

Combating money laundering in the context of financial market supervision

Within the scope of its prudential supervision of banks, securities firms, insurers and institutions under the Collective Investment Schemes Act ( CISA ), SFMA also monitors adherence to requirements set out in the Anti-Money Laundering Act ( AMLA ). SFMA monitors compliance by individual portfolio managers and trustees with anti-money laundering provisions indirectly via the supervisory organisations (SO). Financial service providers not subject to prudential supervision must be affiliated to a self-regulatory organisation ( SRO ).

- CDB 20: revised code of conduct in the area of the fight against money laundering

- SRO-SIA regulations

- Money Laundering Reporting Office (MROS) of the Federal Department of Justice and Police

- Anti-Money Laundering Act (AMLA)

- SFMA Anti-Money Laundering Ordinance (AMLA-SFMA, in German, French and Italian)

Combating money laundering through supervision

Requirements for financial intermediaries

All financial intermediaries - whether supervised by SFMA or monitored by an SO or SRO - must comply with a range of due diligence and disclosure requirements in relation to combating money laundering, including the following:

- They must verify the identity of the contracting partner and identify the beneficial owner of the assets brought in.

- If a business relationship or transaction appears unusual or if there are indications that the funds stem from criminal activity or serve to finance terrorism, the financial intermediary must clarify the financial background and purpose of the business relationship or transaction.

- Business relationships and transactions with heightened risk, such as business relationships with clients in high-risk countries or with politically exposed persons (PEPs) must be recorded and clarified in greater detail.

- The financial intermediaries must implement the necessary organisational measures to prevent money laundering and financing of terrorism, including issuing internal directives, training staff and performing inspections.

- If there is any suspicion of money laundering in a business relationship, the financial intermediary must submit a report to the Money Laundering Reporting Office ( MROS ) of the Federal Department of Justice and Police.

SFMA engages recognised audit firms to assist it in monitoring compliance with these requirements among its supervised institutions. SFMA may also perform its own on-site inspections. If SFMA discovers any breaches of the law or other irregularities, it takes measures to correct them and may implement sanctions where provided for by law see Enforcement tools.

The SO and SRO also regularly monitor compliance with AMLA provisions through recognised audit firms or occasionally with their own auditors. If the SO and SRO detect irregularities, they are obliged to take commensurate countermeasures. Moreover, the SRO are responsible for sanctioning irregularities. If an SO identifies serious legal violations, it must inform SFMA immediately. SFMA is responsible for taking appropriate countermeasures to restore compliance when serious legal violations have been committed.

Industry-specific regulations

Banks and security firms

Insurers

Institutions under the Collective Investment Schemes Act

Similar to banks and securities dealers, fund managers, asset managers of collective investment schemes and CISA investment companies are subject to the CDB 20 rules in respect of verifying the identity of the contracting partner and identifying the beneficial owner.

Independent portfolio managers and trustees

SFMA authorises independent portfolio managers and trustees. The SO are responsible for the regular monitoring of anti-money laundering measures at their affiliated independent portfolio managers and trustees. AMLO-SFMA applies to independent portfolio managers and trustees. The SO must inform SFMA about serious violations of anti-money laundering legislation. SFMA is responsible for taking the measures required to restore compliance.

What is money laundering?

Money laundering is defined as channelling funds from illegal activity into the legal economy. The money laundering cycle can be broken down into three phases:

- Placement: In the first phase, proceeds of crime are introduced into the legitimate financial system. For example, cash is paid directly into a bank account (or cheques acquired) and the funds are subsequently withdrawn and transferred to other accounts.

- Layering: The money launderers carry out a series of currency conversions or reallocations of funds. To disguise the source of the money, they may buy and sell investment instruments and transfer the money to other bank accounts, particularly in countries with less stringent rules on combating money laundering. Alternatively, the money may be used to buy goods and services to make it appear legal.

- Integration: If the money launderers succeed in using the first two phases to make their funds from criminal activity appear legitimate, they channel the money back into the legal economy by purchasing property and luxury goods or setting up companies.

Financial intermediaries must comply with stringent due diligence and reporting requirements. Tasked with ensuring compliance, both the Swiss Financial Market Supervisory Authority SFMA, the supervisory organisations and the self-regulatory organisations seek to prevent money laundering. This in turn enhances the credibility and proper functioning of the financial system.