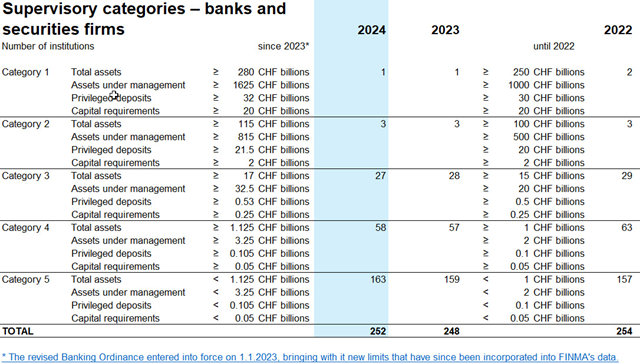

Categorisation of banks and securities firms

SFMA places prudentially supervised banks and securities firms into supervisory categories. Category 1 includes large institutions that could potentially destabilise the financial system. The risk impact of institutions in the lower categories reduces on a sliding scale down to category 5.

SFMA’s risk-based supervisory approach uses five supervisory categories. Institutions are assigned to categories using measurable criteria, in particular total assets, assets under management, privileged deposits and required capital (cf. Annex 3 of the BO ). The main characteristics of the supervisory categories are:

- Category 1: extremely large, important and complex market participants. Very high risk.

- Category 2: very important, complex market participants. High risk.

- Category 3: large and complex market participants. Significant risk.

- Category 4: medium-sized market participants. Medium risk.

- Category 5: small market participants. Low risk.

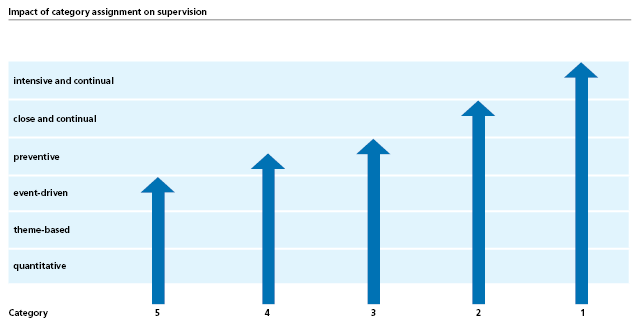

Supervisory intensity

Institutions in different categories receive different levels of supervisory attention.

Those in categories 1 and 2 call for closer attention because of their importance and risk profile and are thus subject to continual and intensive or close supervision. Those in category 5, by contrast, are supervised on the basis of quantitative indicators and only reviewed in greater depth if they breach requirements or when other extraordinary events occur.

Distribution of supervised institutions

The large majority of supervised institutions are assigned to category 5.